新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

P2公司报告(Corporate Reporting)是ACCA财务会计体系中的高级课程,同样也是该体系中的倒计时一门。在F3和F7的基础上,P2要求考生更加深入地掌握会计准则,以及运用相关知识进行财务分析。

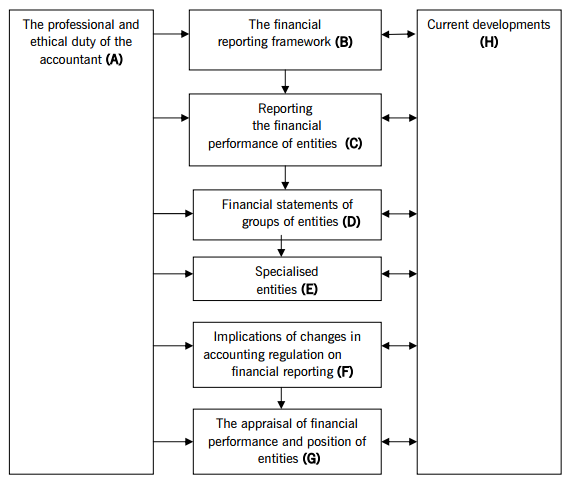

以下为P2大纲的基本框架以及各个知识点间的联系:

RELATIONAL DIAGRAM OF MAIN CAPABILITIES

在ACCA考试中,越到后面的高阶课程,对于知识的灵活运用能力要求越高。在ACCA学习中,尤其在P阶段考试中,要特别注重理论与实际相结合,不要单纯的死背定义,概念,准则内容,要做到灵活全面的学习,要会合理的通过数据去分析案例。对于重点内容,要在脑中建立整体构架,要求对知识体系有全面的把握和清晰的了解,这样才能在审题和做题过程中,保证逻辑清晰,避免出现缺少步骤丢分的情况。

以制作Statement of Financial Position 步骤为例,我们可以通过自己做题或者老师上课所讲内容做出如下步骤图,这样做题时也可以避免缺少步骤,起到事半功倍的效果。

Step1:

Group Structure

Step2:

Individual Adjustment for Sub

Step3:

Net Asset Preparation

(OSE, RE, OCE and Fair Value Adjustment)

Inter Company Trading (URP Adjustment)

Setp4:

Goodwill

Proportion Method

Full Method

Impairment

Step5:

NCI

Proportion Method

Full Method

Impairment

Step6:

Associated/JV (Equity Method)

Step7:

Individual Adjustment (Acquirer)

Balance Sheet and P&L (RE)

Balance Sheet and Equity (OCE)

Step8:

Group RE

Acquirer’s RE balance at Reporting Date

Sub Post Acquisition Profit Sharing (Controlled)

Association Post Acquisition Profit Sharing

Individual Adjustment for Acquirer (P&L related)

Step9:

Group OCE

Acquirer’s OCE balance at Reporting Date

Sub Post Acquisition OCE sharing (Controlled)

Individual Adjustment for Acquirer (Equity Related)

Step10:

Consolidation

Copyright © 2000 - www.fawtography.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载