新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

转移定价(transfer price)知识点在ACCA历年考试中频率很高。一般来说,简单的考核方式会给出一些条件让考生判断产品的外部需求是否已经满足,工厂是否已经满负荷运转,这些情况下应该选用可变成本还是市场价格来定价。做这类题目的时候需要从集团利益的角度的出发,考虑部门之间应该采取内部购销还是各自从外部购入或对外销售。总之,做出的决策和制定的价格既要满足集团的利益又不能影响各部门的绩效考评。下面我们来看一下2011年12月Q2这道例题,虽然年份比较久远,但是非常经典,难度也比较大,可以说考出了F5绩效管理的精髓。

(接 ACCA F5 试题解析:转移定价(transfer price)(一) )

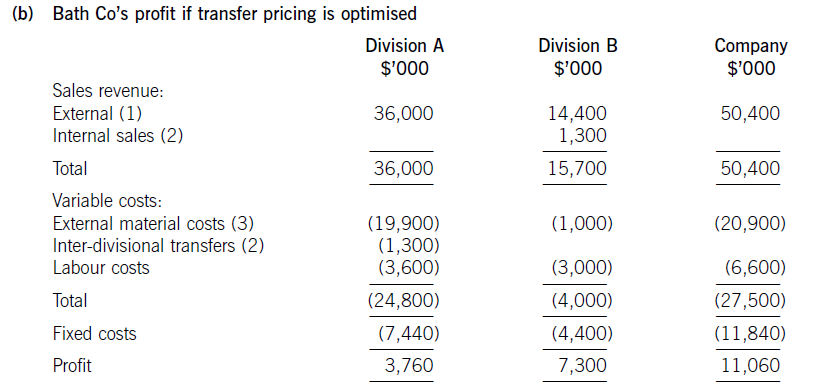

Workings ($’000)

(1) External sales

Div A: 80,000 x $450 = $36,000

Div B: 180,000 x $80 = $14,400

(2) Internal sales/inter-divisional transfers

Div B:20,000 x $65 = $1,300

(3) Material costs

Div A: 60,000 x $265 + (20,000 x $200) = $19,900

Div B: 200,000 x $5 = $1,000

A transfer price of $65 has been used on the assumption that the company will introduce the policy discussed in (c).

Provided that the transfer price is set between the minimum of $20 (Division B’s marginal cost) and $65 (the cost to Division A of buying from outside the group), the actual transfer price is irrelevant in this calculation. The overall profit of the company will be the same.

(b)问需要考虑什么样的转移政策是至优的,所有的采购和销售行为需要从整个集团的角度出发。部门B总产能200,000单位,对外比对内销售赚取的收入更多。从集团利益出发选择优先对外销售180,000, 剩余20,000闲置产能,本着避免内部资源浪费的原则,需要将其出售给部门A。A的需求是80,000单位,剩下60,000选择从外部购置。但是A部门经理更倾向外部采购,因为只需要支付成本65美元,低于内部转移价格75美元,这个时候需要调整一下transfer price来平衡双方的利益。B生产的原材料可变成本包括原材料5美元和人工成本15美元,内部转移的至优定价应该控制在可变成本和市场价格之间,即20美元到65美元。从集团出发,选择20还是65没有区别,因为至终编制合并报表的时候收入成本全部抵消。但是评估各部门绩效的时候会优先选择定价65,对A来说不论内部转移还是外部购买都要花费65美元,对于B来说,它用的闲置产能,只要能够弥补可变成本即可,定价65美元还可以获取一定金额的贡献,这也是B部门愿意看到的结果。

对比(a)和(b)问的结果我们可以看出选择65美元的内部转移价格集团可以获取更多的利润。

(c) Issues and suitable transfer price

Divisional managers’ performance is assessed using a metric as decided by the company. This may simply be the profit for the period, or, depending on the type of responsibility centre being used, a metric such as residual income or return on capital employed. Whatever the metric being used, the division’s profit figure is going to affect it and divisional managers are therefore going to be keen to maximise their individual profits. By focusing on individual decisions, divisional managers are often not aware of the impact of their decisions on the company as a whole. This would particularly be the case where a decision which is in the best interests of the company actually makes an individual division’s performance look worse.

The transfer pricing system in place needs to take into account the behavioural impact of the prices being charged. Sometimes, this can mean that a ‘dual transfer pricing system’ needs to be introduced in order to ensure that divisional managers act in the interests of the company as a whole.

It can be seen from part (b) that the best decision for the company is that:

– Division A buys 60,000 sets of fittings from an outside supplier and buys the remaining 20,000 sets of fittings from Division B in order to ensure that Division B is working to full capacity.

– Division B sells as many sets of fittings as possible externally, at $80 per set. Since the maximum external demand is 180,000 units, Division B sells the remaining 20,000 sets of fittings to Division A. The minimum transfer price that would be acceptable to Division B is its marginal cost of $20 per unit, since it has spare capacity. However, if this transfer price is used, Division B becomes worse off than before the autonomy was given, and Division B’s manager will not like this. As far as Division A is concerned, it will not want to pay more than the $65 that it can buy from outside the group.

Bath Co’s policy therefore needs to ensure that, firstly, Division A’s manager is prepared to buy 20,000 sets of fittings from Division B and secondly, Division B is prepared to sell them at $65 per set. Since it is in Division B’s best interest to work to full capacity and the manager of Division B knows that Division A can obtain fittings for $65 per set, it should not be difficult for B to agree to sell to A at this price. A policy of negotiated transfer prices would achieve this fairly quickly. However, the company also needs to have a policy that divisions buy internally first, where this would be in the best interests of the overall profitability of the company. This would ensure that Division A buys the 20,000 sets of fittings from Division B. This way, the overall profit of the company is maximised whilst also ensuring that divisional managers do not become demotivated.

对部门经理进行绩效考评的时候会基于一些利润指标,比如RI和ROI,可能会出现一些不合理的情况,比如dysfunctional。题目中提到A经理如果有自主权会更倾向于外部采购,但是从集团的利益出发,需要先消化掉B部门的剩余产能,如果按照75元定价则对A不公平,所以倒计时定价为65美元。

制定转移价格时候还可以采用一种更高级的方法“dual pricing”。这时候需要引入Bath集团公司。B可以以80美元的价格先卖给Bath,Bath再卖给A的时候售价20,差额60可以在集团账上记成一笔费用,这样是比较公平的方式。

大家在复习transfer price知识点的时候可以参考本题和2015年6月Q2,通过做题有助于加深对这部分的理解。倒计时,希望大家都能够顺利通过ACCA考试。

网校为广大学生提供免考科目预评估服务,您可以点击![]() 进行评估申请。

进行评估申请。

关注“ACCA考试辅导”微信公众号,获取更多讯息

Copyright © 2000 - www.fawtography.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载