新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

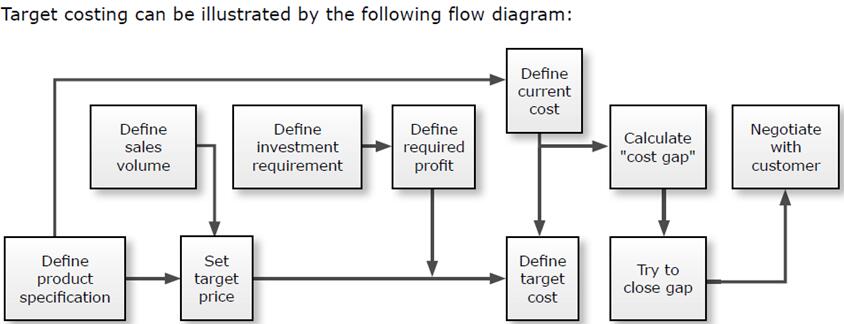

目标成本法 Target Costing

定义:

目标成本法是指以给定的竞争价格为基础,从而决定产品的成本,以保证实现预期的利润。目标成本法的核心工作是制定企业新产品的目标成本,并不断改进产品与工序设计,从而确保新产品的成本小于或等于目标成本。

Target costing is an attempt to achieve an acceptable margin in a situation where the price of a product is determined externally by the market. This acceptable margin is achieved by identifying ways to reduce the costs of producing the product.

目标成本法的步骤:

1. 通过研究市场,确定产品的市场接受度,考虑市场份额;

Determine the price the market will accept for the product, based on market research. This may take into account the market share required.

2. 从价格中扣除必要的利润率,以得到目标成本;

Deduct a required profit margin from this price—this gives the target cost.

3. 预估产品的实际成本。如果是一个新产品,预估成本将是一个估价;

Estimate the actual cost of the product. If it is a new product, this will be an estimate.

4. 设法缩小产品的实际成本和目标成本差距 。

Identify ways to narrow the gap between the actual cost of the product and the target cost.

Copyright © 2000 - www.fawtography.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载