新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

IFRS 15 Revenue from Contracts with Customers

1. Principles of Revenue Recognition

1.1 IFRS 15

IFRS 15 Revenue from Contracts with Customers outlines the five steps of the revenue recognition

process:

Step 1 Identify the contract(s) with the customer

Step 2 Identify the separate performance obligations

Step 3 Determine the transaction price

Step 4 Allocate the transaction price to the performance obligations

Step 5 Recognise revenue when (or as) a performance obligation is satisfied

The core principle of IFRS 15 is that an entity recognizes revenue from the transfer of goods or services to a customer in an amount that reflects the consideration that the entity expects to be entitled to in exchange for the goods or services.

1.2 Identify Contracts With Customers

Def inition:

Contract— an agreement between two or more parties that creates enforceable rights and obligations.

Contracts can be written,verbal or implied based on an entity's customary business practices.

Customer— a party that has contracted with an entity to obtain goods or services that are an output of the entity's ordinary activities in exchange for consideration.

The revenue recognition principles of IFRS 15 apply only when a contract meets all of the following criteria:*

·the parties to the contract have approved the contract;

·the entity can identify each party's rights regarding the goods or services in the contract;

·the payment terms can be identified;

·the contract has commercial substance;and*

·it is probable that the entity will collect the consideration due under the contract.*

1.3 Identify Performance Obligations

Performance obligation a promise to transfer to a customer:

·a good or service (or bundle of goods or services) that is distinct;or

·a series of goods or services that are substantially the same and are transferred in the same way.

If a promise to transfer a good or service is not distinct from other goods and services in a contract,then the goods or services are combined into a single performance obligation.

A good or service is distinct if both of the following criteria are met:

1. The customer can benefit from the good or service on its own or when combined with the customer's available resources;and

2. The promise to transfer the good or service is separately identifiable from other goods or services in the contract.*

*A transfer of a good or service is separately identifiable if the good or service:

·is not integrated with other goods or services in the contract;

·does not modify or customise another good or service in the contract;or

·does not depend on or relate to other goods or services promised in the contract.

1.4 Determine the Transaction Price

Transaction price the amount of consideration to which an entity is entitled in exchange for transferring goods or services.

The transfer price does not include amounts collected for third parties (i.e. sales taxes or VAT).

The effects of the following must be considered when determining the transaction price:

·the time value of money;*

·the fair value of any non-cash consideration;

·estimates of variable consideration;

·consideration payable to the customer.*

Consideration payable to the customer is treated as a reduction in the transaction price unless the payment is for goods or services received from the customer.

1.5 Allocate the Transaction Price

The transaction price is allocated to all separate performance obligations in proportion to the stand-alone selling price of the goods or services.

Def inition

Stand-alone selling price— the price at which an entity would sell a promised good or service separately to a customer

·The best evidence of stand-alone selling price is the observable price of a good or service when it is sold separately.

·The stand-alone selling price should be estimated if it is not observable.

The allocation is made at the beginning of the contract and is not adjusted for subsequent changes

in the stand-alone selling prices of the goods or services.

1.6 Recognise Revenue

·Recognise revenue when (or as) a performance obligation is satisfied by transferring a promised good or service (an asset) to the customer.

·An asset is transferred when (or as) the customer gains control of the asset.

·The entity must determine whether the performance obligation will be satisfied over time or at

a point in time.

2. Performance Obligations

2.1 Satisfied Over Time

·A performance obligation is satisfied over time if one of the following criteria is met:

·The customer receives and consumes the benefits of the entity's performance as the entity performs (e.g. service contracts,such as a cleaning service or a monthly payroll processing service).

·The entity's performance creates or enhances an asset that the customer controls as the asset is created or enhanced (e.g. a work-in-process asset).

·The entity's performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date.

·Revenue is recognised over time by measuring progress towards complete satisfaction of the performance obligation.

·Output methods and input methods (described in s.3) can be used to measure progress towards completion.*

·Revenue for a performance obligation satisfied over time can only be recognised if the entity can make a reasonable estimate of progress.

·Revenue is recognised to the extent of costs incurred if there is no reasonable estimate of progress,but the entity expects to recover its costs.

2.2 Satisfied at a Point in Time

·A performance obligation that is not satisfied over time is satisfied at a point in time.

·Revenue should be recognised at the point in time when the customer obtains control of the asset.

·Indicators of the transfer of control include:

·the customer has an obligation to pay for an asset;

·the customer has legal title to the asset;

·the entity has transferred physical possession of the asset;

·the customer has the significant risks and rewards of ownership;

·the customer has accepted the asset.

2.3 Statement of Financial Position Presentation

·A contract asset or contract liability should be presented in the statement of financial position when either party has performed in a contract.

Definition:

Contract liability— an entity's obligation to transfer goods or services to a customer for which the entity has received consideration from the customer or consideration is due from the customer (i.e. the customer pays or owes payment before the entity performs).

Contract asset— an entity's right to consideration in exchange for goods or services that the entity has transferred to the customer (i.e. the entity performs before the customer pays).

·In addition,any unconditional right to consideration should be presented separately as a receivable in accordance with IFRS 9 Financial Instruments.*

3. Measuring Progress Towards Completion

3.1 Output Methods

·Output methods recognise revenue on the basis of the value to the customer of the goods or services transferred to date relative to the remaining goods or services promised.

·Examples of output methods include:

·Surveys of performance completed to date*

·Appraisals of results achieved

·Milestones achieved

·Time elapsed

·Units produced or delivered.

*The value of “work certified” to date may be a measure used to identify the degree of completion and therefore revenue to be recognised in profit or loss. Work certified is an output method and a term that was used under previous standards.

·Output methods should only be used when the output selected represents the entity's performance towards complete satisfaction of the performance obligation.*

*A disadvantage of output methods is that the outputs used may not be available or directly observable. When this is the case,an input method may be necessary.

3.2 Input Methods

·Input methods recognise revenue on the basis of the entity's efforts or inputs to the satisfaction of the performance obligation relative to the total expected inputs.*

·Examples of input methods include:

·Resources consumed

·Labour-hours worked

·Costs incurred

·Time elapsed

·Resources consumed.

·Revenue can be recognised on a straight -line basis if inputs are used evenly throughout the performance period.

3.3 Cost Recognition

·Costs associated with a contract whose performance obligation is satisfied over time are expensed as and when they are incurred;they are not recognised on a proportional basis.

·Therefore,if revenue is measured using an output method,prof it recognition will be volatile for contracts that straddle two or more accounting periods.*

·If an incurred cost is not proportionate to the progress in the satisfaction of the performance obligation that cost shall be excluded when measuring the progress of the contract.

·In this situation revenue will be recognised to the extent of the actual cost incurred in respect of that component.

4 Recognition of Contract Costs

4.1 Incremental Costs of Obtaining a Contract

Incremental costs of obtaining a contract costs to obtain a contract that would not have been incurred if the contract had not been obtained.

·The incremental costs of obtaining a contract,such as sales commissions,are recognised as an asset if the entity expects to recover them.

·Costs to obtain the contract that would have been incurred regardless of whether the contract was obtained are charged to expense when incurred.

4.2 Costs to Fulfil a Contract

·Costs incurred to fulfil a contract that are not within the scope of another standard should be recognised as an asset if they meet all of the following criteria:

·They relate directly to a contract;

·They generate or enhance the resources of the entity;and

·They are expected to be recovered.

·Costs that must be expensed when incurred include:

·General and administrative costs;

·Cost of wasted materials,labour or other resources;and

·Costs that related to satisfied performance obligations.

5 Specific Transactions

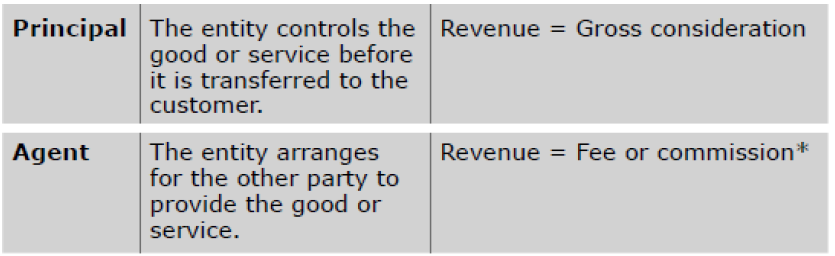

5.1 Principal v Agent

·When an entity uses another party to provide goods or services to a customer,the entity needs to determine whether it is acting as a principal or an agent.

The fee or commission may be the net consideration that the entity retains after paying the other party the consideration received in exchange for the good or service.

·Indicators that an entity is an agent and does not control the good or service before it is provided to the customer include:

·Another party is responsible for fulf illing the contract;

·The entity does not have inventory risk;

·The entity does not have discretion in establishing prices for the other party's goods or services;

·The consideration is in the form of a commission;and

·The entity is not exposed to credit risk.

5.2 Repurchase Agreements

Repurchase agreement a contract in which an entity sells an asset and also promises or has the option to repurchase the asset.

·There are three forms of repurchase agreements:

1. An entity's obligation to repurchase the asset (a forward);

2. An entity's right to repurchase the asset (a call option);

3. An entity's obligation to repurchase the asset at the customer's request (a put option).

5.2.1 Forward or Call Option

·When an entity has an option or right to repurchase an asset,the customer does not obtain control of the asset and the entity accounts for the contract as either:

·a lease if the entity can or must repurchase the asset for less than the original selling price;or

·a financing arrangement if the entity can or must repurchase the asset for an amount greater than or equal to the original selling price.

·If the repurchase agreement is a financing arrangement,the entity will:

·continue to recognise the asset;

·recognise a financial liability for any consideration received from the customer;and

·recognise as interest expense,which increases the financial liability,equal to the difference between the amount of consideration received from the customer and the amount of consideration to be paid to the customer.

5.2.2 Put Option

·If an entity has an obligation to repurchase the asset at the customer's request for less than the original selling price,the entity accounts for the contract as either:

·a lease,if the customer has a significant economic incentive to exercise the right;or

·a sale with a right of return,if the customer does not have a significant economic incentive to exercise the right.

·If the repurchase price is equal to or greater than the original selling price,the entity accounts for the contract as either:

·a financing arrangement,if the repurchase price is more than the expected market value of the asset; or

·a sale with a right of return,if the repurchase price is less than or equal to the expected market value of the asset and the customer does not have a significant economic incentive to exercise the right.

5.3 Bill-and-Hold Arrangements

Bill-and-hold arrangement a contract in which the entity bills a customer for a product that it has not yet delivered to the customer.

·Revenue cannot be recognised in a bill-and-hold arrangement until the customer obtains control of the product.

·Generally,control is transferred to the customer when the product is shipped to the customer or delivered to the customer (depending on the terms of the contract).*

·For a customer to have obtained control of a product in a bill-and-hold arrangement,all of the following criteria must be met:

·There must be a substantive reason for the bill-and hold arrangement (e.g. the customer has requested the arrangement because it does not have space for the product);

·The product has been separately identified as belonging to the customer;

·The product is currently ready for transfer to the customer;and

·The entity cannot use the product or direct it to another customer.

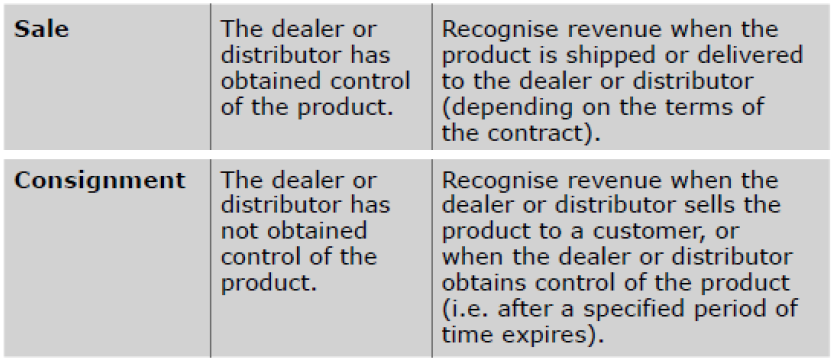

5.4 Consignments

·When an entity delivers its product to a dealer or distributor for sale to end customers,the entity needs to determine whether the contract is a sale or a consignment arrangement.

The following are indicators of a consignment arrangement:

·The entity controls the product until a specified event occurs,such as the sale of the product to a customer or until a specified period expires.

·The entity can require the return of the product or transfer the product to another party.

·The dealer does not have an unconditional obligation to pay the entity for the product (although it might be required to pay a deposit).

编辑推荐:ACCA P2(INT)考试内容变化

下一篇:ACCA9月考试时间

Copyright © 2000 - www.fawtography.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载