新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

QUANTIFIABLE BENEFITS

Here, the extent of the benefits or improvements can be forecast. It is only once benefits have become quantifiable that there is any hope of progressing to financial measurement and the construction of a sound economic business case for the project. There are several challenges:

· Ensuring that all quantifiable benefits and costs are captured. If an important factor is omitted, then the analysis will be distorted.

· Establishing a starting point – a baseline against which changes can be compared. This requires measurement techniques to be established.

· Predicting the changes that the project will cause – turning measurable changes into quantifiable changes.

Ward and Daniel offer suggestions for transforming measurable to quantifiable:

· Pilot operations. For example, implement a new inventory system in one branch and carefully monitor results. Extrapolate changes company-wide.

· External benchmarking. Monitor what other industry members are achieving using their approaches. If possible, monitor the best-in-class performance. If a rival performs better and uses a particular approach to business, then there might be evidence there about how our performance would change.

· Reference sites. External benchmarking is not available for changes that are relatively new to an entire industry because there are few comparisons available. However, unless a company is absolutely the first, often reference sites will exist where suppliers have persuaded another organisation to be an early adopter of new technology or methods. Some care is needed here as, obviously, suppliers will not readily provide information about their failures.

· Modelling and simulation. For example, if an organisation has a sophisticated financial model on a spreadsheet, then different assumptions can be introduced and the results quickly seen. Call centres keep very careful records of queuing times and the number of callers who hang-up before being attended to. They can extrapolate with some confidence the effect of reducing waiting times.

· Historical internal data. This is particularly relevant to organisations thinking about stopping an activity. It is important that their cost data is accurate so that the true implications of ceasing an activity are properly quantified. Activity-based costing is almost certainly more relevant than the conventional treatment of fixed overheads.

FINANCIAL BENEFITS

Once changes have been quantified, it should be a reasonably easy step to convert those to financial effects. It is important that this is done – at least for profit-seeking organisations – and that the calculations are not distorted to ensure that a project is improperly justified. Typically, net present value or return on capital calculations will be used to evaluate the financial effects. Sensitivity analysis will be an essential part of the exercise to identify risk areas and plan for more investigative work to be done there.

PLANNING OF BENEFITS REALISATION

Planning of benefits realisation means:

· assigning dates by which defined benefits should be enjoyed

· detailing the implementation and change management procedures needed to ensure that the expected benefits are actually achieved as fully as possible

· establishing dates and methodologies for measurement of the benefits for subsequent comparison to plans.

Note that the opportunities for benefit creation will start with completing the various parts of a project (its activities) on time, within budget, to the correct quality standards, and focused accurately on previously agreed outcomes. However, although each part of a project can be properly delivered, the project as a whole can fail to produce benefits unless it is whole-heartedly embraced by key stakeholders. For example, a technically excellent new website could be implemented, but if customers choose not to use it then few benefits will arise.

CARRYING OUT THE PROJECT, KEEPING IT UNDER CONSTANT REVIEW

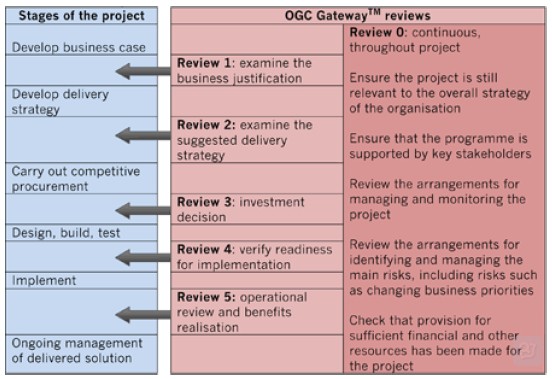

The Office of Government Commerce (OGC) is an independent office of the UK Treasury, established to help government deliver best value from its spending. The OGC has developed the OGC Gateway (TM) Process in which projects are examined at various key decision points before they are allowed to progress to the next stage. This UK-based example is indicative of a formal system of project implementation and review where evaluation takes place at several gateway points to ensure that the original business case, the project objectives and expected benefits continue to be achieved.

The OGC Gateway (TM) Process can be represented as follows:

After the project business case is established, Gateway’s review 1 would be carried out to examine the justifications and arguments presented. The reviewing board will be looking for benefits and disbenefits that might have been overlooked or assumptions that appear to be unrealistic.

If all is well, the project will go forward to the next stage in which a detailed delivery strategy is worked out. The ‘Who? How? When? What?’ questions are addressed here. For example:

· Who will be on the project team?

· How much will be subcontracted?

· What exactly will be delivered and by when?

Review 2 will look critically at these decisions and objectives. Only when the reviewing board is satisfied that the project is sufficiently well-defined and specified will it give the go-ahead to receive tenders from outside suppliers.

After the competitive tenders have been received, the next stage will be signing a supply contract and committing the organisation to substantial expenditure. Before that is done, Review 3 will look at the tenders received, their costs, the standing and competence of the suppliers and whether – now that costs are known more accurately – the project still offers value for money (net benefits).

Assuming the supply contract is signed, then investment in the project will start. It could be an IT project requiring software design, writing and testing; it could be a project to reorganise the structure and reporting lines of the company; it could be a project to merge with a rival organisation. However, before action is taken and the software or plans are implemented, it is important to review what is proposed. There is no point in trying to implement proposals that are not-tested, incomplete or poorly designed. So Review 4 will look at the project plans and see if they are sufficiently robust and comprehensive to attempt to implement. It will also be necessary to ensure that the organisation is ready for implementation of the plans.

Review 5 then looks at the results that the project is delivering. Have the expected benefits materialised? If not, then why not? Can shortfalls in benefits or unexpected disbenefits be corrected? Review 5 could be carried out several times as the new solution gradually settles down and management problems are ironed out.

Note carefully the purpose of Review 0. This should be carried on continuously throughout the project and is there to keep questioning whether the original business case on which the project was predicated remains valid. No matter how meticulously a project is managed, changing events can suddenly undermine a business case. For example, a project to build a new factory can suddenly look uneconomic if the economy suffers a sharp fall. Or, further investment in a project might be pointless if its completion seems to be in jeopardy because funds have become very tight.

REVIEWING THE RESULTS

After a project has been implemented, there are three types of review that should be performed, reflecting different perspectives.

· A post-project review. This examines how the project went in terms of how the project team and how the project manager performed and identifying what aspects of planning and review went well and what didn’t go so well. Was the project completed within time and budget? The focus here is on the project. Lessons learnt are fed back into the project management system. For example, if the project estimation was poor, then better methods of estimation might be integrated into the project management process to help ensure that future estimates are more accurate.

· A post-implementation review. This is essentially the Gateway review 5 and it examines what the project achieved (its product or outcome) and should compare the post-implementation observations and measurements with the hoped-for benefits that were the basis of the original business case. As part of this review, it

· will be important to gather information from key stakeholders. The initial focus here is on the product or outcome produced by the project. Does it meet its objectives? Lessons learnt are fed back into the product production process – for example, in the development of a website, technical mistakes might be fed back into the software development process to help ensure that they do not happen again in the future.

· Benefits realisation is a type of post-implementation review. It focuses on the realisation of the anticipated business benefits. As mentioned before, it could be performed several times, reflecting the expected benefits timing defined in the formal investment appraisal. A product might be successfully delivered (for example, a new website or the merger of two organisations); however, the anticipated business benefits may not be delivered. Lessons learnt in benefits realisation are fed back into the benefits management process. For example, this could lead to better ways of classifying benefits. It is important to recognise that an appropriate product might be delivered (a website), but the anticipated business benefits may never accrue. The reasons for this have to be investigated and understood. Perhaps the initial business case was over-optimistic or perhaps external business factors have changed that prevent the business benefits from being delivered.

Without these reviews, an organisation will be condemned to repeating any mistakes it may have made and will be unable to make use of any lessons learned.

Ken Garrett is a freelance author and lecturer

Reference (1) Benefits Management: Delivering Value from IS and IT Investments, John Ward and Elizabeth Daniel, Wiley, 2006.

Copyright © 2000 - www.fawtography.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载